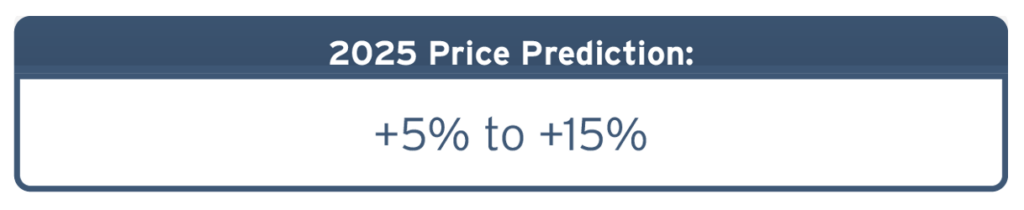

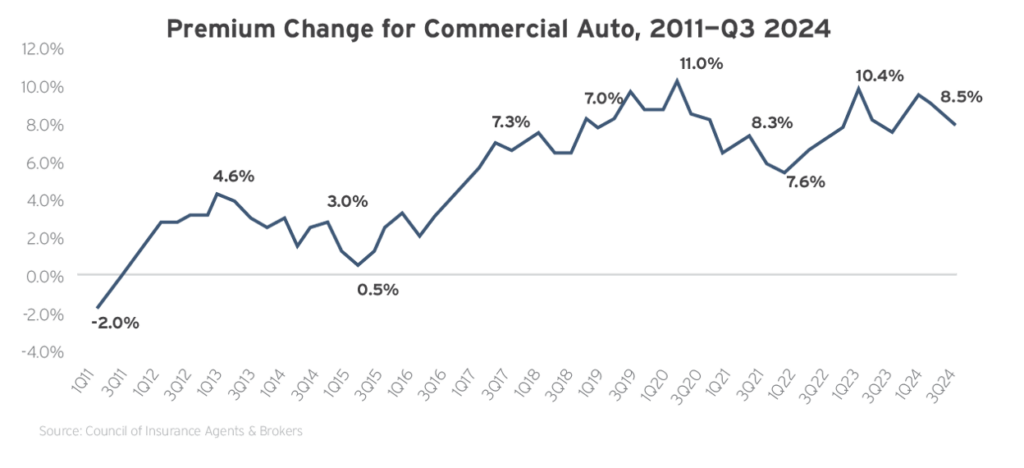

For much of the past decade, the commercial auto insurance market has been especially challenging for both insurers and insureds, characterized by significant underwriting losses, plummeting profitability and continued rate hikes. In 2024, commercial auto insurance premiums had some of the highest increases across all lines of insurance, with average increases between 9% and 9.8% in the first two quarters of the year. What’s more, as of 2024, insurers have experienced combined loss ratios above 100% for 12 of the past 13 years, and insurers are paying out more in claims and expenses than they are earning in premiums.

This trend is expected to continue into 2025. Various factors have led to such difficult market conditions, including widespread driver shortages, nuclear verdict concerns, inflation issues and distracted driving challenges. Altogether, these cost-driving trends have pushed claims frequency and exacerbated overall loss severity throughout the segment.

As a result, policyholders with large commercial fleets and additional auto exposures have had greater difficulty securing excess layers of coverage alongside elevated program pricing. In response, some businesses are adapting their operations in an attempt to lower their insurance expenses (e.g., changing their radius of operation by shifting from long-haul to local trucking or using smaller box trucks instead of tractors for long-distance hauling). Considering these developments, most insureds—regardless of industry or vehicle class—can expect to encounter ongoing premium hikes going into 2025. Further, policyholders with sizeable fleets or poor loss history may be more susceptible to double-digit rate jumps, reduced capacity and possible coverage restrictions.

Developments and Trends to Watch

Nuclear verdict concerns

Social inflation refers to the rising cost of insurance claims due to increased litigation, broader definitions of liability and more friendly legal environments. It has affected many lines of commercial coverage in recent years, with the commercial auto insurance market being one of the hardest hit. This sector is particularly susceptible to nuclear verdicts (e.g., extremely high jury awards) due to the serious nature of accidents involving large commercial vehicles like trucks. According to the American Transportation Research Institute, trucking verdicts have increased by more than 50% each year for the past decade, with nuclear verdicts in the sector doubling during this time frame. From 2019-23, the average statutory closed claim payment for commercial auto liability cases increased by 39%. The upward frequency of claims and the rise in litigation costs, average settlements and third-party litigation funding continue to create an uphill battle for insurers and their book of business. In total, the Insurance Information Institute reported that the culmination of social inflation and nuclear verdicts has led to a $30 billion surge in commercial auto claim costs since 2012. Moreover, driven by social inflation, liability claims in the United States have increased by 57% in the last 10 years. On average, social inflation rose by 5.4% annually from 2017-22, peaking at 7% in 2023 to reach a 20-year high.

Due to the rise in nuclear verdicts, attorneys are more inclined to go to trial, which typically extends litigation and significantly raises the cost of defending a claim. Third-party litigation funding is also contributing to this trend. This funding occurs when a third party provides financial support for a lawsuit and, in exchange, receives a portion of the settlement. In the past, the steep cost of attorney fees would often scare plaintiffs away from taking a lawsuit to trial. But now, with litigation funding, a third party covers most or all costs associated with the litigation, leading to more cases being pursued. Not only is litigation funding becoming more common, but it also increases the cost of litigation overall—sometimes to seven figures. This is because plaintiffs can take cases further and seek larger settlements. The ongoing surge in nuclear verdicts has caused many commercial auto insurance carriers to either decrease their risk appetites and restrict coverage offerings or exit the market altogether. Consequently, insureds affected by nuclear verdicts are less likely to have sufficient coverage for these events, potentially leading to financial devastation when they occur. While tort reform at the state level could provide some relief from litigation challenges (i.e., caps on noneconomic damages), commercial auto insurance buyers should expect the current environment around nuclear verdicts to persist in 2025.

Physical damage claims

The overall cost associated with vehicle collisions has climbed significantly in recent years. While the financial impact of individual accidents can vary based on the severity of a collision, steep repair costs continue to drive up the cost of claims overall. Technological advancements have made vehicles safer and more efficient. However, as commercial vehicles are outfitted with a variety of sophisticated components (e.g., backup cameras and blind-spot cameras), they are becoming increasingly expensive to repair. According to a report from AAA, vehicles equipped with driver assistance systems often cost twice as much to repair as those that aren’t. As such, losses associated with a collision are much more substantial, leading to rate increases and creating numerous challenges for insurers. Continued supply chain issues have also contributed to higher repair costs. Notably, repair shops are experiencing delays in obtaining parts (e.g., microchips), driving up repair times and downtime for commercial fleets. Given the cost and time it takes to repair vehicles, a collision can be especially expensive for a commercial fleet. More often, the threshold for declaring a vehicle a total loss is reached more quickly, especially considering that the combined cost of repairs and a vehicle’s salvage value commonly exceeds the actual cash value of the vehicle as a whole. In response to these challenges, some companies are likely to continue streamlining practices related to preventive maintenance, towing, rental car provision and parts ordering.

Driver shortages

While labor shortages have become a top concern for many industries in recent years, the transportation sector has been particularly impacted by a lack of commercial drivers. While an estimated 3.05 million truck drivers were employed in the United States in 2023, the American Trucking Associations (ATA) estimates a shortage of roughly 60,000 drivers in 2024, with the shortage expected to grow to 82,000 by the end of the year. What’s worse, the ATA anticipates that rising freight demand and an aging workforce could cause the driver shortage to skyrocket to 160,000 open positions by the end of the decade.

To help minimize this shortage, a growing number of businesses have adjusted their driver recruitment and retention strategies. This has included offering higher wages, improving working conditions, providing professional growth opportunities and tapping into underrepresented demographics (e.g., women) to expand their talent pools. Yet, many businesses have still had to lower their driver applicant standards to fill open positions. These drivers often have fewer years of experience and shorter driving records. Such factors can make these new employees more likely to be involved in accidents on the road, contributing to an increase in commercial auto losses and related claims. In order to combat risks stemming from inexperienced drivers, the federal government introduced the DRIVE Safe Integrity Act in May 2023. This bipartisan legislation aims to enhance safety and training standards for both new and current drivers, as well as promote the adoption of a permanent apprenticeship program for young commercial drivers who are just starting their careers in transportation. Even with these regulatory efforts underway, it’s clear that it’s increasingly important for employers to establish their own initiatives to educate new drivers and encourage them to prioritize safety behind the wheel next year and beyond, thus minimizing accidents and associated losses.

Fleet electrification

Electric vehicles (EVs) continue to gain traction in the U.S. auto market, including among commercial fleets. According to a recent report, there were over 1 million EVs in commercial and government fleets as of 2021—an increase of over 233% from 2019 estimates. By 2030, experts estimate there will be over 4 million EVs in U.S. fleets. The increased adoption of EVs in the commercial auto space may be attributed to decreased battery costs, expanded charging infrastructure, government incentives, sustainability initiatives and regulatory pressures. However, EV adoption isn’t without its share of challenges. In one Accenture survey, 35% of respondents cited high up-front costs and an unclear return on investment as challenges toward fleet electrification. That same survey found that 30% of respondents didn’t currently have any EVs in their fleet. Infrastructure upgrades could also slow down EV initiatives for some fleets, as the change may require electrical system upgrades, specialized charging equipment and updates to the organization’s IT systems. Further, because EVs tend to cost more than standard automobiles, their insurance rates are usually higher. However, other factors unique to EVs could also make insuring them costlier. Such factors include:

- Cyberthreats—Like most new cars and trucks, EVs offer connected car technologies such as Wi-Fi, data sharing and semiautonomous systems that leave them vulnerable to cyberthreats. However, the public charging stations EVs rely on to recharge their batteries add another layer of risk. Charging stations may serve as an entry point for malware attacks, data theft, system outages, bugs and glitches. What’s more, once a data breach occurs in a single vehicle, it may be easier for a malicious party to access the rest of the fleet.

- Battery problems—There are several risks associated with EV batteries that can potentially impact commercial fleets. For example, battery manufacturing defects can lead to large-scale vehicle recalls, putting fleet owners at an increased risk of business delays. Additionally, under certain conditions, lithium-ion batteries that power EVs can ignite or explode. Battery fires burn longer and hotter, release more toxic fumes and liquids, and spread faster over a larger area than traditional fires. Such an incident would create a whole new set of insurance challenges.

- Pedestrian accidents—One selling point of EVs is they run quieter than gasoline-powered vehicles. Unfortunately, this lack of audible engine noise may also put pedestrians at greater risk of being hit if they fail to hear an approaching EV.

- While uncertainty about new EV technologies will likely drive up insurance premiums initially, expectations are that prices will stabilize over the long term.

Tips for Insurance Buyers

- Examine your risk management practices relative to your fleet and drivers. Enhance your driver safety programs by implementing or modifying policies on safe driving.

- Design your driver training programs to fit your needs and your business’s exposures. Establish effective onboarding and educational initiatives for new drivers. Regularly retrain drivers on safe driving techniques.

- Ensure you are hiring qualified drivers by using motor vehicle records (MVRs) to vet a driver’s past experience and moving violations. Disqualify drivers with an unacceptable driving record. Review MVRs regularly to ensure that drivers maintain good driving records. Define the number and types of violations a driver can have before losing their driving privileges.

- Evaluate and integrate advanced vehicle technology solutions, such as telematics, GPS tracking and dash cameras, to bolster your current loss control practices.

- Implement an employee retention program to maintain experienced drivers.

- Prioritize organizational accident prevention initiatives and establish effective post-accident investigation protocols to prevent future collisions on the road.

- Examine your Federal Motor Carrier Safety Administration BASIC scores to identify gaps in your fleet management programs, if applicable.

- Comply with applicable commercial driving legislation, particularly as it pertains to road safety, vehicle maintenance and drug testing policies.

- Determine whether you should make structural changes to your commercial auto policies by speaking with trusted insurance professionals.

Read the Complete 2025 Market Outlook Series

- Commercial Property Insurance

- General Liability Insurance

- Commercial Auto Insurance

- Workers’ Compensation Insurance

- Cyber Insurance

- D&O Insurance

- Employment Practices Liability Insurance

Want more information? Contact Us. We’d be happy to walk you through any of these topics and all your risk management needs.