In recent years, the commercial property insurance market has been characterized by rising premiums and years of double-digit rate increases. 2023 was one of the more challenging years on record, and the segment saw average rate hikes above 20% for the first time in more than 20 years.

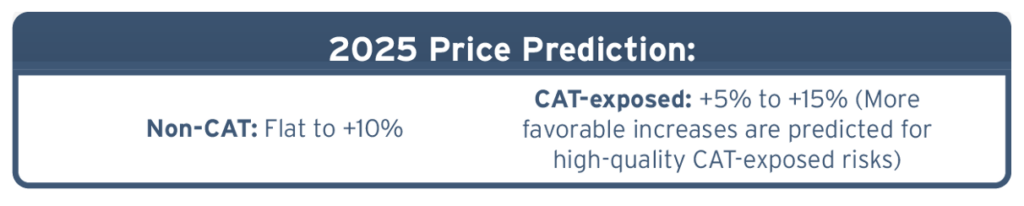

Moving into 2025, the market appears to be stabilizing, and most renewals with favorable loss histories will see single-digit rate increases; non-catastrophe (CAT) exposed assets with good loss histories can expect flat to 10% rate increases. While some complex risk profiles are still difficult to place and challenges remain in high-risk areas with persistent capacity and pricing pressures (e.g., wildfire zones), the double- or triple-digit rate increases the commercial property insurance segment saw in 2023 are less common.

This improvement is largely due to improved capacity, healthier returns on capital, and a renewed focus on data and risk quality. Although the market appears to be more stable and competitive, updated CAT models may affect the risk appetite of insurers and lead to pricing fluctuations. In general, insureds in wildfire and hurricane-prone areas should expect fewer coverage options and higher rates in 2025; however, difference-in-condition and parametric policies may help mitigate risk and address coverage gaps.

Developments and Trends to Watch

Natural disasters

The frequency and severity of natural disasters have continued to pose concerns throughout the commercial property insurance market. Through October 2024, this year saw 24 weather and climate disasters with losses exceeding $1 billion, according to the National Oceanic and Atmospheric Administration. These included 17 severe storms (e.g., tornados, windstorms and hailstorms), four tropical cyclones, one wildfire and two winter storms. Altogether, these events resulted in 418 deaths and significant damage. Severe convective storms have significantly contributed to overall losses from natural disasters. These storms occur when warm, moist air rises rapidly, resulting in the formation of tornadoes, hail, severe thunderstorms and strong winds. As of the third quarter of 2024, insured losses from natural disasters reached approximately $108 billion, with severe convective storms being the primary cause. Hurricane Helene incurred insured losses estimated between $10 billion and $15 billion, making it the costliest event in the year’s first nine months. Furthermore, projected losses from Hurricane Milton are expected to range from $30 billion to $60 billion. Overall, total insured losses for 2024 are anticipated to exceed $140 billion, indicating another year of significant financial impact from natural disasters.

A stable reinsurance market and increased capacity

In previous years, the surge in extreme weather events, substantial underwriting losses and prolonged inflation proved especially challenging for the commercial property reinsurance segment. These trends generated some degree of market uncertainty and earnings volatility, prompting some reinsurers to reduce or even eliminate capacity for CAT exposures. The 2023 market cycle was quite chaotic, as primary insurers faced significant increases in reinsurance costs, higher attachment points and more restrictive terms. However, the reinsurance market stabilized in 2024 and is expected to recover close to pre-COVID-19-pandemic highs. This surge has been fueled by increased involvement from capital markets through instruments such as insurance-linked securities, CAT bonds and sidecar arrangements, resulting in significant growth in available capacity. Additionally, higher retentions by policyholders—as they take on the financial responsibility of smaller, more frequent claims—have contributed to lower losses for reinsurers. The increased access to reinsurance capital has enabled direct insurers to offer more stable and increased capacity for renewals or new business. High-risk accounts are taking advantage of increased capacity through shared and layered programs from international markets like London and Bermuda. Effectively, insurers have more capital available and are willing to take on portions of larger, more complex risks, making it easier for some insureds to secure coverage.

Insurance-to-value (ITV) considerations

ITV calculations are critical, as they help insureds determine the appropriate amount of property coverage by assessing an asset’s actual, market and replacement value. Securing an accurate ITV calculation has been challenging; a property’s value is often affected by factors like inflation and material costs, both of which have been volatile in recent years. However, inflation appears to be cooling, per a September 2024 report from the U.S. Bureau of Labor Statistics. The consumer price index came in at 2.4%—the lowest inflation rate since February 2021. Given these market changes, it’s crucial that insureds are diligent in ITV calculations. An accurate ITV calculation represents as close to an equal ratio as possible between the amount of insurance a business obtains and the estimated value of its commercial building or structure, thus ensuring adequate protection following potential losses. According to recent industry research, many businesses’ ITV calculations are off by more than 30%, presenting major coverage gaps. To avoid inaccurate valuations and insufficient coverage, insurance experts recommend using the replacement value of a property when conducting ITV calculations. This value is an estimate of the current cost to replace or rebuild a property. The replacement value of a property depends on characteristics such as material and labor expenses, architect services, debris removal needs and building permit requirements. Common approaches to accurately estimating this value include getting a property appraisal from a third-party firm, leveraging fixed-asset records that have been adjusted for inflation or relying on a basic benchmarking tool (e.g., dollars per square foot).

Continued interest in alternative risk financing

Given how challenging the commercial property insurance market has been in recent years due to factors such as inflation and pervasive natural disaster concerns, there’s been continued interest in alternative risk transfer options. These can provide more customized solutions and, in some cases, cost savings. There are several options available to risk managers, including the following:

- Captives—Captives are insurance companies formed by one or more parent companies to insure their own risks rather than relying on third-party insurers. They are a form of alternative risk transfer used by major corporations, nonprofit organizations and medium-sized businesses to achieve better control over their insurance needs, manage costs and gain potential tax benefits. By creating a captive, a company can often lower its total cost of risk through more tailored risk management and claims handling processes. Captives can be formed to handle various types of risks, depending on the exposures of the parent organization.

- Parametric coverage—As natural disasters become more severe, parametric coverage has risen in popularity. Contrary to the reimbursement method of standard commercial policies, parametric insurance offers protection based on a predetermined, measurable characteristic tied to a covered event. Under such coverage, the amount a policyholder is compensated isn’t decided by the exact cost of damages sustained but by the calculated intensity of the covered event itself. For instance, if a hurricane caused damage to a commercial property, a parametric policy might reimburse a set dollar amount linked to the storm’s wind speeds. Key advantages of this coverage include the ability to remedy possible property insurance gaps posed by large-scale natural disasters, more timely payouts (often less than three weeks) using simplified proof-of-loss protocols, and greater policy flexibility and transparency. According to industry data, submission volume in the parametric segment has jumped by 500% over the last year, with the market projected to nearly triple in value and exceed $29 billion by 2031.

- Structured fronting—Structured fronting is an insurance solution that allows insureds to manage their own risk. In these arrangements, policies are written by an insurer, but most or all the risk is passed on to the insured or another third party (e.g., a captive or reinsurer). This allows insureds to meet regulatory obligations tied to having a licensed insurer issue a policy. Structured fronting offers policyholders flexibility in managing coverage and risk retention, allowing them to customize their insurance arrangement to better align with their risk management goals.

Tips for Insurance Buyers

- Conduct a thorough inspection of your commercial property and the surrounding area for specific risk management concerns. Implement additional mitigation measures as needed.

- Work with insurance professionals to begin the renewal process early. Many commercial property insurers are seeing an increased submission volume. Timely, complete and quality submissions are vital to ensure your application will be reviewed by underwriters.

- Determine whether you should adjust your organization’s commercial property limits to avoid underinsuring your property and facing coinsurance penalties. This may entail updating your total insurable values as needed and conducting accurate ITV calculations.

- Gather as much data as possible regarding your existing risk management techniques. Be sure to work with your insurance professionals to present loss control measures you have in place.

- Analyze your organization’s natural disaster exposures. If your commercial property is located in an area that is more prone to a specific type of catastrophe, implement mitigation and response measures that will protect your property as much as possible if such an event occurs (e.g., installing storm shutters on windows to protect against hurricane damages or utilizing fire-resistant roofing materials to protect against wildfire damages).

- Develop a documented business continuity plan (BCP) that will help your organization remain operational and minimize damages in the event of an interruption. Test this BCP regularly with various possible scenarios. Make updates when necessary.

- Report commercial property claims to your insurance carrier as soon as possible and, if applicable, take action to limit the damage caused by these claims.

- Address insurance carrier recommendations. Insurers will be looking at your loss control initiatives closely. Taking the appropriate steps to reduce risks whenever possible can make your business more attractive to underwriters.

- Keep your commercial property in good condition at all times and address building issues that could lead to insurance claims immediately.

Read the Complete 2025 Market Outlook Series

- Commercial Property Insurance

- General Liability Insurance

- Commercial Auto Insurance

- Workers’ Compensation Insurance

- Cyber Insurance

- D&O Insurance

- Employment Practices Liability Insurance

Want more information? Contact Us. We’d be happy to walk you through any of these topics and all your risk management needs.