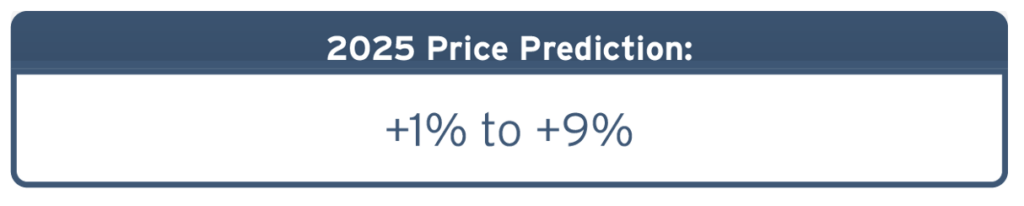

Following years of rising claim frequency and severity, as well as poor underwriting results, the general liability insurance market showed signs of improvement in 2024. Rate increases for general liability customers moderated, and many insureds saw premium hikes below 10%—a vast improvement over the double-digit rate increases from previous years. For most policyholders, price increases in 2024 remained in the 4%-5% range.

However, like other segments in the commercial insurance space, hard market conditions are expected for businesses that operate in riskier industries or have poor loss histories. Some sectors, like construction, affordable housing and hospitality, remain especially challenging due to their inherent risks and high exposure to litigation.

In addition, hedge funds and other financiers are more often investing in law firms that specialize in liability lawsuits, fueling a litigious environment with substantial financial backing. These firms use aggressive advertising on billboards, social media and TV commercials to promote awareness of potential payouts. Alongside these marketing tactics, well-funded firms employ litigation strategies designed to extend the legal process, such as filing extensive motions, pushing for broad discovery and strategically delaying proceedings. This approach often drives up claim costs, increases the likelihood of trials, and leads to larger verdicts and settlements. Consequently, claims that might have once been resolved informally are now more frequently taken to court, with rising numbers of individuals seeking compensation after accidents or injuries. Together, these trends are contributing to a surge in liability lawsuits and adding upward pressure on insurance costs.

For 2025, insurers will continue to focus on underwriting profitability and risk management. While capacity is healthy, general liability insurers will continue to be cautious about who they insure and at what price. Renewal results will likely depend on policyholders’ unique exposures, class and loss history. To secure favorable rates and terms, insureds should focus on demonstrating strong risk management practices.

Developments and Trends to Watch

Litigation concerns

The United States is an increasingly litigious society, leading to a growing number of lawsuits following liability incidents (actual or alleged) and, in turn, greater settlements and verdicts from such legal action. This trend, driven by social inflation (growth in insurance claim costs due to a more litigious environment and changing attitudes towards lawsuits), has driven up the frequency and severity of claims in the commercial general liability market. Key factors contributing to this environment include increased attorney advertising, third-party litigation funding (TPLF), and the rise of nuclear verdicts and settlements—awards that exceed $10 million.

Attorney advertising has become more widespread, spanning television, print and social media, and highlights opportunities to pursue legal action across various scenarios—thus fueling litigation against businesses. Moreover, the global TPLF industry, which allows third parties to invest in lawsuits by financing attorneys or plaintiffs in exchange for a share of any settlement, is projected by industry experts to reach $30 billion by 2028. By providing financial backing to cases that might otherwise be too costly to pursue, TPLF enables more cases to proceed, often extending litigation and increasing the likelihood of trials, which frequently lead to larger verdicts and higher claim costs.

Nuclear verdicts are also on the rise, particularly in the case of class-action lawsuits. According to independent public relations firm Marathon Strategies, between 2020 and 2022, the average nuclear verdict nearly doubled from $21.5 million to $41.1 million, while the sum of these verdicts jumped from $4.9 billion to $18.3 billion in the same time frame. Plaintiffs’ attorneys have become more adept at maximizing jury awards, leveraging tactics like reptile theory and anchoring. Reptile theory is a trial strategy designed to appeal to a juror’s primal instincts of safety, positioning defendants as a threat to the community, while anchoring involves suggesting high—and often unreasonable—initial damages amount to influence the final award. These tactics have proven especially effective with younger jurors, such as millennials and Generation Z, who tend to be more skeptical of corporations and sympathetic to plaintiffs.

Altogether, increased litigation, rising verdicts and surging social inflation issues have largely contributed to elevated general liability insurance claim costs. In some cases, such litigation has posed underinsurance concerns for businesses, leaving them with coverage gaps and substantial out-of-pocket expenses amid associated claims. This challenging legal environment is expected to persist, making it essential for businesses to proactively manage their risks and secure appropriate coverage in 2025.

Biometric data losses

Many businesses are increasingly using biometric data, such as facial geometry, iris scans, fingerprints and voiceprints, to enhance account authentication measures, deploy stricter access controls, create personalized marketing materials, and monitor employees’ workplace attendance and activities. While biometric data can allow organizations to maintain greater operational visibility and provide stakeholders with more individualized experiences, it also carries risks related to data privacy and personal security.

The regulatory landscape for biometric data collection is constantly evolving, paving the way for potential challenges for businesses. While no overarching federal law applies specifically to biometric data in the United States, some aspects of federal legislation regulate certain sectors and individuals (e.g., the Health Insurance Portability and Accountability Act and the Children’s Online Privacy Protection Act). More comprehensive data privacy laws have emerged at the state level, and at least 10 states have recently proposed such laws.

Even though it may be challenging, organizations must comply with applicable data privacy laws. Failure to adhere to relevant legislation when collecting biometric data could be deemed wrongful, leaving noncompliant organizations subject to legal penalties ranging from thousands to millions of dollars in fines and strict sanctions. Compounding these expenses, organizations that engage in improper biometric data collection, processing, sharing or storage practices could also be susceptible to costly litigation brought on by disgruntled stakeholders, especially if their data gets compromised.

Many businesses subject to biometric data lawsuits seek coverage under the “personal and advertising injury” provisions of their general liability policies, as they traditionally cover privacy violations. However, many insurers frequently contest these claims, resulting in inconsistent court outcomes. In response to this uncertainty, the Insurance Services Office recently updated its commercial general liability exclusions, adding “biometric information” to the list of protected data and introducing endorsements that exclude coverage for violations of certain biometric data laws.

Considering these risks, employers should prioritize compliance and risk mitigation next year to effectively navigate the risks of biometric data collection. Businesses should seek legal counsel, review their policy language and consider alternative insurance options (e.g., cyber coverage), which may offer more tailored protection against biometric data losses.

Active assailant exposures

An active assailant incident occurs when an individual or group of individuals enter a populated area to kill or attempt to kill their victims, generally through the use of firearms. These events—sometimes called active shooter incidents or mass shootings—have skyrocketed in the United States. According to the most recent data from the FBI, there were 229 active shooter incidents from 2019-23—an 89% increase from the previous five-year period. These incidents have also grown in severity; 3 out of the 5 deadliest mass shootings in U.S. history occurred in the past decade.

Active assailant incidents can carry numerous consequences and often result in fatalities, serious injuries and prolonged emotional trauma among those involved. Additionally, such incidents can leave lasting impacts on organizations. Specifically, businesses that encounter active shooter incidents could face substantial recovery expenses, regulatory penalties and liability concerns. Courts increasingly hold businesses accountable if an organization doesn’t take the appropriate steps to protect against an active assailant, potentially finding them negligent and in breach of their duty of care should they be subject to lawsuits. In response to this risk, some businesses have started to more carefully evaluate their active assailant exposures, implement loss control measures and create incident response plans.

In response to these growing risks, businesses are turning to specialized insurance policies designed to cover losses related to active shooter incidents. While these policies vary in design, they often include coverage for property damage, business interruption, third-party liability, crisis management, psychological counseling, funeral expenses, risk assessment, training and medical expenses. This type of coverage is especially critical, as standard general liability policies often exclude coverage for certain types of violent acts or claims related to mental anguish or emotional trauma. Therefore, standalone active assailant coverage or specific policy endorsements may be essential for financial protection.

Perfluorosulfonic acids (PFAS) exposure

PFAS consist of a large grouping of over 7,000 chemicals that have been widely manufactured and distributed across the United States since the 1940s. Because PFAS don’t break down easily within the environment or the human body, these substances are known as “forever chemicals.” PFAS can be present in various products, including food packaging, nonstick cookware, household cleaners, firefighting agents, textiles, furniture and auto parts. Over the past few years, PFAS have been the subject of growing scrutiny stemming from recent developments regarding the health and safety of these substances and their environmental impacts. Namely, PFAS have been linked to several health conditions, including certain cancers and immune dysfunction. As more information regarding the risks of PFAS comes to light, regulatory issues involving these substances have ensued.

Although two main types of PFAS (i.e., perfluorooctanoic acid and perfluorooctane sulfonate) have already faced regulatory action—resulting in these substances no longer being manufactured in the United States since 2015 and 2002, respectively—the federal government recently implemented multiple efforts to limit PFAS usage and exposure in the coming years and beyond. Such efforts include creating national water quality standards related to PFAS contamination, designating certain PFAS as hazardous substances, enhancing PFAS reporting requirements, limiting PFAS discharge from industrial sources, and conducting and publishing toxicity assessments for various PFAS. Apart from federal legislation, several states currently have standards restricting PFAS contamination in soil and groundwater. Additionally, New York and New Jersey have already listed PFAS as hazardous substances within their regulatory regimes.

This legislation has contributed to a rise in litigation and subsequent liability concerns for businesses that are found responsible for causing PFAS contamination amid their operations. For instance, multiple manufacturers have faced lawsuits due to their operations resulting in contaminated soil or drinking water and allegedly leading to health complications in individuals located near their worksites. While recent PFAS litigation has been directed primarily at manufacturers, it’s certainly possible that businesses across additional industries could encounter lawsuits related to the use of these substances in their products and packaging, prompting liability claims and associated losses. What’s worse, many carriers have begun excluding coverage for PFAS-related losses from their general liability policies. As regulatory pressures and litigation concerns related to such chemicals press on into 2025, businesses that manufacture PFAS, sell products containing these substances or utilize packaging with PFAS may experience elevated liability exposures. Further, businesses facing PFAS-related incidents could be more susceptible to coverage exclusions and out-of-pocket losses.

Claims stemming from PFAS incidents pose unique challenges for general liability insurers and insureds, particularly given that coverage is typically triggered when the injury or damage happens, not when a claim is filed. Because PFAS exposure often happens gradually and over an extended period, it can take years or even decades for claims to arise. Legacy policies issued before the mid-1980s may provide broader coverage for PFAS claims, given they often lack pollution exclusions; however, this would require insureds to locate so-called “lost policies” in order to address PFAS liabilities. Policies written more recently are likely to have absolute pollution exclusion, which can make it difficult to secure coverage for PFAS claims.

Tips for Insurance Buyers

- Work with risk management experts to educate yourself on key market changes affecting your rates and how to respond using loss control measures.

- Adopt proactive safety and risk management measures to minimize incidents that could lead to lawsuits, such as employee training and stringent safety protocols. Create an active assailant response plan that includes evacuation procedures, staff training and communication protocols to mitigate and protect employees.

- Keep detailed records of your company’s protocols and risk management measures to streamline the claims or litigation process. Documentation, such as written policies, training logs, inspection records and incident reports, can serve as valuable evidence that your business has taken reasonable steps to reduce risk.

- Communicate transparent data collection practices to employees and customers, ensuring they understand how their biometric data will be used and stored.

- Create workplace policies and procedures aimed at minimizing PFAS exposures. Consult legal counsel to ensure compliance with applicable PFAS legislation.

- Examine your general liability coverage with trusted insurance professionals to ensure your policy terms and limits match your insurance needs, and consider adding endorsements where needed.

Read the Complete 2025 Market Outlook Series

- Commercial Property Insurance

- General Liability Insurance

- Commercial Auto Insurance

- Workers’ Compensation Insurance

- Cyber Insurance

- D&O Insurance

- Employment Practices Liability Insurance

Want more information? Contact Us. We’d be happy to walk you through any of these topics and all your risk management needs.