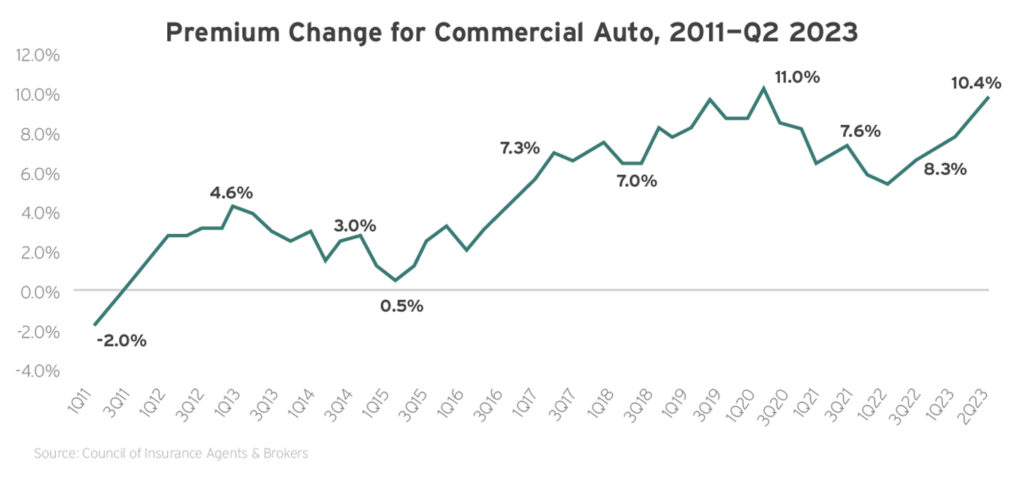

The commercial auto insurance market has faced hardening conditions for much of the past decade, as evidenced by significant underwriting losses, plummeting profitability and continued rate hikes. Although 2022 saw lower average premium increases due to strengthening reserves and 2021’s combined ratio falling below 100 for the first time in several years, this deceleration wasn’t here to stay.

According to credit rating agency AM Best, 2022’s combined ratio jumped back up to 105, representing $3.3 billion in underwriting losses. In response to this poor market performance, industry data revealed that average rate jumps reached 8% in the first half of 2023. By the latter half of the year, the majority of policyholders experienced premium increases near or above double digits.

Various factors have led to such difficult market conditions, including widespread driver shortages, nuclear verdict concerns, inflation issues and distracted driving challenges. Altogether, these cost-driving trends have pushed claims frequency to pre-pandemic levels and exacerbated overall loss severity throughout the segment. As a result, policyholders with large commercial fleets and additional auto exposures have had greater difficulty securing excess layers of coverage alongside elevated program pricing. Considering these developments, most insureds—regardless of industry or vehicle class—can expect to encounter ongoing premium hikes going into 2024. Further, policyholders with sizeable fleets or poor loss history may be more susceptible to double-digit rate jumps, reduced capacity and possible coverage restrictions.

2024 Price Prediction: +5% to +30%

Developments and Trends to Watch

Driver shortages

While labor shortages have become a top concern for many industries in recent years, the transportation sector has been particularly impacted by a lack of commercial drivers. According to the American Trucking Associations (ATA), the nation’s driver shortage totaled 64,000 open positions in 2023 and is forecasted to reach a record high of 82,000 in 2024. What’s worse, the ATA anticipates that rising freight demand and an aging workforce could cause the driver shortage to skyrocket to 160,000 open positions by the end of the decade. To help minimize this shortage, a growing number of businesses have adjusted their driver recruitment and retention strategies, including offering higher wages, improving working conditions, providing professional growth opportunities and tapping into underrepresented demographics (e.g., women) to expand their talent pools. Yet, many businesses have still had to lower their driver applicant standards to fill open positions. These drivers often have fewer years of experience and shorter driving records. Such factors can make these new employees more likely to be involved in accidents on the road, contributing to an increase in commercial auto losses and related claims.

In order to combat risks stemming from inexperienced drivers, the federal government introduced the DRIVE Safe Integrity Act in May 2023. This bipartisan legislation aims to enhance safety and training standards for both new and current drivers, as well as promote the adoption of a permanent apprenticeship program for young commercial drivers who are just starting their careers in transportation. Even with these regulatory efforts underway, it has become increasingly important for businesses to establish initiatives of their own to educate new drivers and encourage them to prioritize safety behind the wheel, thus minimizing accidents and associated losses.

Nuclear verdict concerns

Social inflation has affected many lines of commercial coverage in recent years; however, the commercial auto insurance market has seen some of the most devasting impacts. This is mainly due to trends in the trucking industry, including a surge in nuclear verdicts. According to the ATRI, trucking verdicts have increased by more than 50% each year for the past decade, with nuclear verdicts in the sector doubling during this time frame. Furthermore, a recent report from the U.S. Chamber of Commerce Institute for Legal Reform found that auto accidents account for nearly one-quarter (22.8%) of all nuclear verdicts across litigation types, with the mean auto accident-related nuclear verdict sitting at $33.8 million. In total, the Insurance Information Institute (III) reported that the culmination of social inflation and nuclear verdicts has led to a $30 billion surge in commercial auto claim costs since 2012. Due to the rise in nuclear verdicts, attorneys are more inclined to go to trial, which typically extends litigation and significantly raises the cost of defending a claim. Making matters worse, the ongoing surge in nuclear verdicts has contributed to many commercial auto insurance carriers either decreasing their risk appetites and restricting coverage offerings or exiting the market altogether. Consequently, insureds affected by nuclear verdicts are less likely to have sufficient coverage for these events—potentially leading to financial devastation when they occur.

Marijuana legalization considerations

The last five years have seen a growing number of states legalize marijuana. Currently, 24 states have legalized recreational marijuana, and 38 have legalized medicinal use; however, this substance is still illegal at the federal level. As marijuana legalization continues to evolve and state and federal laws remain at odds with each other, this substance has presented a range of risks for businesses. Namely, such legalization could increase the likelihood of commercial drivers operating vehicles under the influence of marijuana, which has been proven to impair decision-making skills, coordination and reaction time. In turn, marijuana legalization could lead to a rise in accidents on the road and related commercial auto losses. To mitigate this risk, the U.S. Department of Transportation (DOT) prohibits drivers from using marijuana behind the wheel and requires them to submit to routine drug testing, with failed tests potentially resulting in adverse employment actions (e.g., license disqualification, suspension or termination).

Nevertheless, recent research revealed that many commercial drivers no longer support the DOT’s marijuana requirements and want testing procedures to change. According to a report from the American Transportation Research Institute (ATRI), more than 100,000 commercial drivers tested positive for marijuana and were removed from their roles between 2020 and 2022. Among these drivers, nearly three-quarters (73%) were still in prohibited status as of 2023 after failing to comply with the DOT’s return-to-duty protocols following a failed drug test, suggesting that those who test positive for marijuana are opting to leave the industry rather than go through the process of regaining their driving eligibility. What’s more, the ATRI’s report found that 72.4% of drivers support “loosening” marijuana laws and testing policies, while 66.5% want the substance legalized at the federal level. Altogether, this means that continued enforcement of the DOT’s requirements could end up exacerbating existing driver shortages and associated commercial auto exposures across the transportation sector.

Inflation issues

In addition to social inflation, general inflation issues have impacted the commercial auto insurance segment in several ways over the last few years. Specifically, inflation has driven up the cost of various auto parts and associated vehicle repair expenses. According to the BLS, vehicle repair prices jumped 23% between 2022 and 2023, nearly quadrupling the average inflation rate. This rise in costs stems from continued advancements in vehicle technology, fluctuating demand for auto parts, global shipment disruptions, labor shortages and ongoing supply chain complications. Apart from increasing auto part and vehicle repair expenses, inflation has also exacerbated the cost of treating third-party injuries following accidents on the road. Namely, prices for medical equipment, surgical procedures and other advanced treatment methods have all climbed. As a whole, inflation issues have compounded commercial auto claim costs and premiums. In fact, a recent III report revealed that inflation has led to claim expenses across the segment totaling an estimated $95 billion to $106 billion higher than they otherwise would have throughout the past decade.

Evolving technology

Vehicles have continued to grow more advanced and incorporate new technology (e.g., blind-spot cameras, backup alarms, GPS devices and other sensors) in recent years, providing opportunities to increase driver safety and bolster operational efficiency among commercial fleets. Automatic braking technology and advanced driver-assistance systems have also risen in popularity, offering features such as lane departure warnings, blind spot detection, and front and rear crash prevention. Smartphones have even begun pushing road safety by providing more hands-free features, deploying “driving mode” options that silence notifications behind the wheel and offering various safe driving applications. When implemented correctly, this technology has the potential to significantly reduce accidents on the road and minimize related costs and insurance claims for businesses with commercial vehicles and drivers.

Tips for Insurance Buyers

- Examine your risk management practices relative to your fleet and drivers. Enhance your driver safety programs by implementing or modifying policies on safe driving.

- Design your driver training programs to fit your needs and the exposures facing your business. Establish effective onboarding and educational initiatives for new drivers. Regularly retrain drivers on safe driving techniques.

- Ensure you are hiring qualified drivers by using motor vehicle records (MVRs) to vet a driver’s past experience and moving violations. Disqualify drivers with an unacceptable driving record. Review MVRs regularly to ensure that drivers maintain good driving records. Define the number and types of violations a driver can have before losing their driving privileges.

- Consider vehicle technology solutions where appropriate to strengthen and supplement other loss control measures.

- Implement an employee retention program to maintain experienced drivers.

- Prioritize organizational accident prevention initiatives and establish effective post-accident investigation protocols to prevent future collisions on the road.

- Examine your Federal Motor Carrier Safety Administration BASIC scores to identify gaps in your fleet management programs, if applicable.

- Comply with applicable commercial driving legislation, particularly as it pertains to road safety, vehicle maintenance and drug testing policies.

- Determine whether you should make structural changes to your commercial auto policies by speaking with trusted insurance professionals.