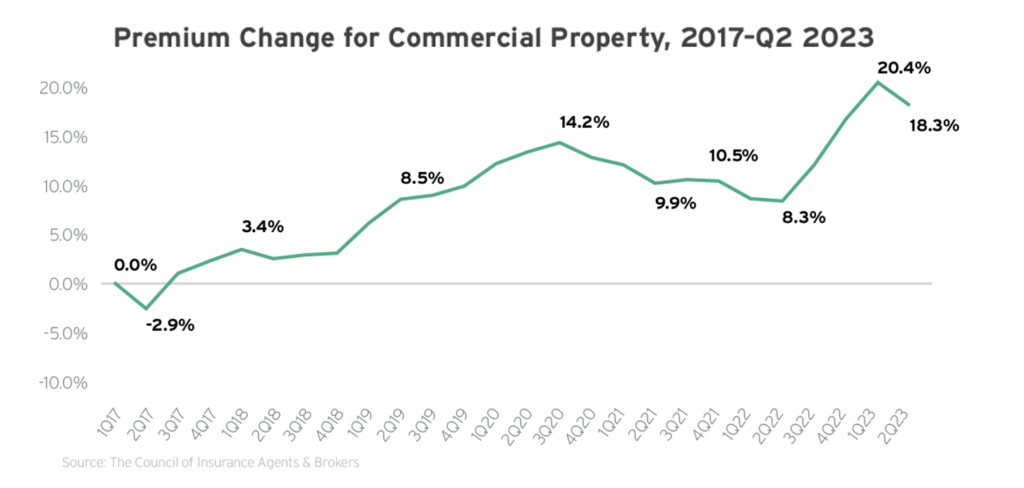

The commercial property insurance market has faced rising premiums since 2017. While such rate jumps showed some signs of slowing in 2022 by largely remaining within single digits, this moderation didn’t last in 2023. According to industry data, commercial property insurance premiums surged by an average of 20.4% in the first quarter of 2023 alone, representing the first time the segment has seen average rate hikes above 20% in more than 20 years.

In the latter half of the year, these rate increases persisted; the segment recorded the highest average premium jumps across all lines of commercial coverage at 18.3%. Industry data also confirmed that the commercial property reinsurance market has been particularly challenging this past year, with rate increases ranging between 25% and 100% for primary insurers exposed to CAT losses.

These unfavorable market conditions are primarily the result of another intense season of natural disasters, inflation issues and an increasingly volatile property valuation landscape. Losses stemming from these trends have forced commercial property insurance carriers to continue elevating the majority of policyholders’ premiums and introducing more restrictive coverage terms. Looking ahead, insureds who conduct high-risk operations, have poor property management practices or are located in natural disaster-prone areas will likely remain susceptible to ongoing rate hikes and coverage limitations.

2024 Price Prediction

- CAT-free: +5% to +15%

- CAT-exposed: +15% to +25%

Developments and Trends to Watch

- Natural disasters—Extreme weather events often leave behind severe property damage and associated losses for affected establishments. As such, the rising frequency and severity of these catastrophes have continued to pose concerns throughout the commercial property insurance market. According to research platform Bloomberg Intelligence, 2023 marks the fourth consecutive year in which global insured losses resulting from natural disasters are projected to exceed $100 billion. Stateside, the NOAA confirmed that the United States experienced a record number of billion-dollar weather and climate disasters in 2023, with the total cost of these events sitting at more than $57 billion. Disasters such as Tropical Storm Hilary, Hurricane Idalia and the Hawaii firestorm were particularly devastating. In addition, convective storms (e.g., thunderstorms, tornadoes and hailstorms) surged across the country this past year. In fact, industry research found that severe thunderstorms contributed to 68% of all weather-related losses in the first half of 2023, costing $35 billion and nearly doubling the 10-year average. Further, the National Interagency Fire Center reported that more than 43,000 wildfires burned over 2.3 million acres nationwide during 2023, destroying thousands of structures. Making matters worse, many climate experts predict that natural disaster trends will continue to exacerbate commercial property losses in the future.

- Inflation issues—Like other lines of coverage, the commercial property insurance segment has been significantly impacted by inflation issues in recent years, prompting higher premiums and claim expenses when losses occur. These issues have been brought on by a combination of fluctuating material demand, supply chain complications, surging prices for various building resources and rising labor costs across the construction sector. Although increased material costs and wage growth trends have certainly softened since their peak in 2021, they continue to exceed pre-pandemic levels, thus affecting property repair and replacement expenses and related claims. According to construction software company Gordian, the price of building materials such as insulation, electrical conduit and concrete jumped by more than 10% in 2023, while the cost of wood and steel increased by over 15%. Additionally, employment website Indeed reported that construction sector wage growth reached 4.4% in 2023, up from 3.6% in 2019. As inflation issues press on in 2024, businesses may not only face increased rates and elevated claim costs following commercial property losses but could also encounter underinsurance concerns due to outdated property valuations. In other words, businesses that don’t update their property values to reflect inflation trends could receive reduced payouts and coinsurance penalties amid commercial property losses, which may result in larger out-of-pocket expenses.

- Insurance-to-value (ITV) considerations—In light of current inflation issues, ensuring accurate property valuations has proven to be a difficult feat. After all, these valuations are tied to the latest building material prices, which have become more volatile over the years. In response to inflation issues affecting building expenses and valuations, insurance experts are encouraging businesses to be more diligent in performing correct ITV calculations and maintaining ample commercial property coverage; some carriers have even introduced specific ITV standards for their policyholders. An accurate ITV calculation represents as close to an equal ratio as possible between the amount of insurance a business obtains and the estimated value of its commercial building or structure, thus ensuring adequate protection following potential losses. According to recent industry research, many businesses’ ITV calculations are off by more than 30%, presenting major coverage gaps. To avoid inaccurate valuations and insufficient coverage, insurance experts recommend using the replacement value of a property when conducting ITV calculations. This value is an estimate of the current cost to replace or rebuild a property. The replacement value of a property depends on characteristics such as material and labor expenses, architect services, debris removal needs and building permit requirements. Common approaches to accurately estimating this value include getting a property appraisal from a third-party firm, leveraging fixed-asset records that have been adjusted for inflation or relying on a basic benchmarking tool (e.g., dollars per square foot).

- Reinsurance capacity challenges—The surge in extreme weather events, substantial underwriting losses and prolonged inflation issues have proven especially challenging for the commercial property reinsurance segment to navigate. Specifically, as natural disasters become more severe and inflation sits at elevated levels, reinsurers are facing a rise in claims, larger investment losses, diminished profitability and reduced capital. For instance, between 2021 and 2022 alone, industry research confirmed that climate-related underwriting losses across the commercial insurance space almost quadrupled. These trends have generated some degree of market uncertainty and earnings volatility, motivating reinsurers to reevaluate whether their existing methods for pricing CAT risks are effectively modeled. Consequently, some reinsurers have lowered capacity for CAT exposures or eliminated capacity altogether. Certain reinsurers have also introduced sublimits and revised their policy wording to establish more distinct coverage limitations. According to industry data, the first quarter of 2023 saw capacity for additional reinsurance coverage layers decrease by more than 50% while rates spiked by 40% to 100%. By midyear renewals, capacity continued to tighten as rates jumped by 25% to 40%. Although demand for reinsurance remains high, capacity will likely become further constrained in 2024, therefore impacting overall commercial property insurance rates, particularly among CAT-exposed policyholders.

Tips for Insurance Buyers

- Conduct a thorough inspection of both your commercial property and the surrounding area for specific risk management concerns. Implement additional mitigation measures as needed.

- Work with insurance professionals to begin the renewal process early. Many commercial property insurers are seeing an increased submission volume. Timely, complete and quality submissions are vital to ensure your application will be reviewed by underwriters.

- Determine whether you will need to adjust your organization’s commercial property limits to avoid underinsuring your property and facing coinsurance penalties. This may entail updating your total insurable values as needed and conducting accurate ITV calculations.

- Gather as much data as possible regarding your existing risk management techniques. Be sure to work with your insurance professionals to present loss control measures you have in place.

- Analyze your organization’s natural disaster exposures. If your commercial property is located in an area that is more prone to a specific type of catastrophe, implement mitigation and response measures that will protect your property as much as possible if such an event occurs (e.g., installing storm shutters on windows to protect against hurricane damages or utilizing fire-resistant roofing materials to protect against wildfire damages).

- Develop a documented business continuity plan (BCP) that will help your organization remain operational and minimize damages in the event of an interruption. Test this BCP regularly with various possible scenarios. Make updates when necessary.

- Report commercial property claims to your insurance carrier as soon as possible and, if applicable, take action to limit the damage caused by these claims.

- Address insurance carrier recommendations. Insurers will be looking at your loss control initiatives closely. Taking the appropriate steps to reduce risks whenever possible can make your business more attractive to underwriters.

- Keep your commercial property in good condition at all times and address building issues that could lead to insurance claims immediately.